How Markets Are Responding to Trade Policies and Rate Expectations

The financial markets are constantly placing bets on where the Federal Funds Rate will land months—even years—into the future. These bets shift with every economic report, policy announcement, and geopolitical headline, making rate expectations a moving target.

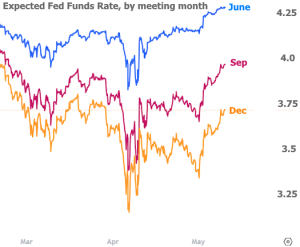

One thing to remember: rate changes don’t happen all at once. If markets anticipate the Fed will cut rates, those cuts are expected to happen in stages. For instance, futures contracts tied to the Fed’s June meeting often show a different outlook than those tied to December. And lately, those differences have been front and center.

Trade Talks Shake Up Rate Forecasts

When the Trump administration first announced new tariffs, markets quickly priced in the potential for faster rate cuts—possibly as soon as May or June. However, after a temporary 90-day pause in the tariff rollout, expectations for near-term cuts backed off. Longer-term outlooks, though, still leaned toward lower rates.

Interestingly, this week’s Fed meeting had little impact on expectations. That’s because the Fed did what everyone expected—reiterating that future rate decisions depend heavily on how trade policies affect the economy. In short:

-

Strong growth and inflation? That’s bad news for rates (they’ll likely rise).

-

Weak growth and less inflation? Good news for rates (they’ll likely fall).

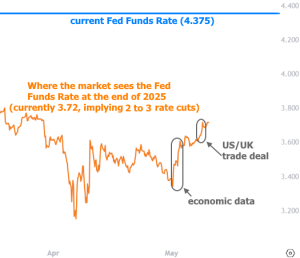

The Fed’s tone may not have shifted, but markets did. Expectations for the year-end Fed Funds Rate finally moved above pre-tariff levels, primarily due to stronger economic data late last week and news of a trade deal between the U.S. and U.K. This movement is clearly visible in the chart below, which focuses on December rate expectations:

Even with this upward movement, expected rates are still significantly below today’s actual rate levels—suggesting the market is still pricing in two to three quarter-point cuts before the year is out.

Mortgage Rates: A Different Story

It’s important to remember that mortgage rates and the Fed Funds Rate are only distantly related. They’re part of the same economic “family tree,” but their behavior often diverges.

For example, while Fed rate expectations have ticked higher since early April, mortgage rates have actually drifted lower.

In fact, when you zoom out to view rates over the past 2–3 years, the pattern looks less like a trend and more like a long, sideways waiting game.

Even before the latest trade developments, rates were stuck in this same holding pattern—waiting for a clear signal from the economy, inflation, and government borrowing trends.

What’s Next?

The coming week could bring some clarity. On deck:

-

Consumer Price Index (CPI): This is the first big inflation reading for April. While it’s too early to fully see the impact of the tariff changes, economists will be watching closely for surprises. A move from 0.1% to 0.3% in core inflation (month-over-month) would be the “no surprise” baseline. Any upside surprise could push rate expectations even higher.

-

US-China Trade Talks: While a quick resolution like the UK deal is unlikely, any major headlines could rattle markets and move rates. These negotiations, combined with inflation data, offer two key sources of potential rate volatility in the week ahead.

Bottom Line:

We’re still in a waiting game. But shifts in trade policy and inflation data could start to shape the next chapter. For now, mortgage rates remain historically favorable, even as the broader rate environment shows signs of movement. Stay tuned—this story is far from over.